For many Americans, retiring at 55 sounds like a dream. The idea of leaving the workforce early and spending more time with family, traveling, pursuing hobbies, or simply enjoying greater freedom is certainly appealing.

But can you actually retire at 55?

The answer depends on several factors, including your savings, expected expenses, healthcare costs, investment strategy, and retirement income sources. While there’s no universal retirement number, understanding the key considerations can help you determine whether early retirement is realistic for your situation.

Let’s walk through the steps.

Step 1: Determine How Much You’ll Spend in Retirement

Before evaluating your savings, it’s important to understand your expected retirement expenses.

Many people assume their spending will decrease significantly in retirement. While certain costs may decline, others can increase, particularly healthcare and travel expenses.

Consider expenses such as:

- Housing

- Utilities

- Healthcare

- Insurance

- Travel and leisure

- Taxes

- Inflation

A good starting point is reviewing your current spending and estimating how those expenses may change once you’re no longer working.

Step 2: Calculate Your Retirement Income Gap

Retiring at 55 presents a unique challenge because you’ll likely need to fund several years before Social Security benefits become available.

Ask yourself:

- How much income will I need each year?

- How much income will my investments need to generate?

- Will I have a pension?

- Will I have rental income or other income sources?

For example, if you need $80,000 annually and expect no pension income, your portfolio may need to generate the majority of that income until other sources become available.

Understanding this gap is critical when evaluating retirement readiness.

Step 3: Evaluate Your Retirement Savings

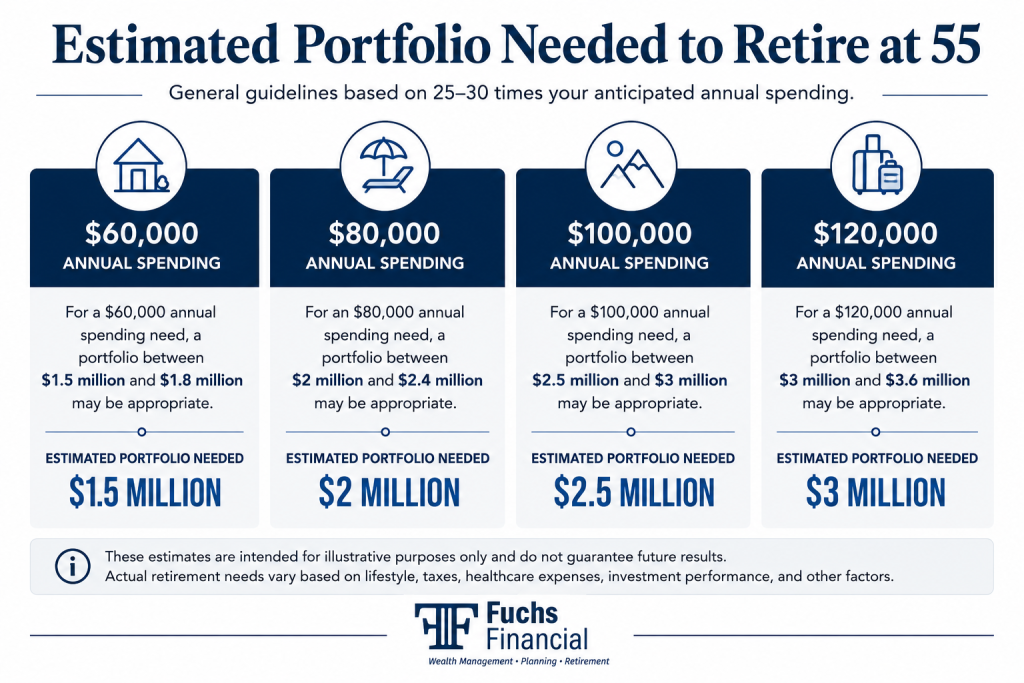

One of the most common questions we hear is, “How much do I need to retire at 55?”

While every situation is different, many financial professionals suggest accumulating approximately 25 to 30 times your anticipated annual spending.

These figures are intended as general guidelines and should not be viewed as guarantees.

Your specific retirement needs will depend on your goals, lifestyle, taxes, investment returns, and other factors.

Step 4: Consider Healthcare Costs Before Medicare

One of the biggest challenges for early retirees is healthcare.

Medicare generally does not begin until age 65. If you retire at 55, you’ll need to bridge a 10-year healthcare gap.

Potential options include:

- Employer-sponsored retiree healthcare

- COBRA coverage

- Affordable Care Act marketplace plans

- Private insurance coverage

Healthcare expenses can be significant, so it’s important to incorporate them into your retirement projections.

Step 5: Understand When Social Security Will Begin

While retiring at 55 may be possible, Social Security benefits generally cannot begin until age 62.

Claiming benefits early can result in permanently reduced monthly payments.

As part of your retirement strategy, consider:

- When you plan to claim benefits

- How claiming age impacts lifetime income

- How Social Security fits into your overall retirement income plan

For more information, read our guide on When to Claim Social Security.

Step 6: Create a Sustainable Withdrawal Strategy

Retirement isn’t simply about reaching a savings target. It’s also about creating a strategy that helps your assets last.

A withdrawal strategy should account for:

- Market volatility

- Inflation

- Taxes

- Required minimum distributions (RMDs)

- Unexpected expenses

Many retirees benefit from having a coordinated plan that balances growth, income generation, and risk management.

Step 7: Evaluate Taxes Before You Retire

Taxes don’t disappear in retirement.

Withdrawals from traditional IRAs and 401(k) accounts are generally taxable, which can impact your retirement income strategy.

Before retiring at 55, consider:

- Future tax brackets

- Roth conversion opportunities

- Tax-efficient withdrawal strategies

- Capital gains considerations

Common Signs You May Be Ready to Retire at 55

While every situation is unique, you may be in a stronger position to retire early if:

- You have little or no consumer debt

- Your mortgage is paid off or nearly paid off

- You have a well-funded emergency reserve

- You have a retirement income plan

- You understand your healthcare options

- Your portfolio can support your desired lifestyle

Most importantly, you’ve evaluated both the financial and emotional aspects of retirement.

The Bottom Line

Retiring at 55 is possible for some individuals, but it requires careful planning and preparation.

The decision should be based on more than a retirement account balance. Healthcare costs, taxes, income needs, Social Security timing, and investment strategy all play important roles in determining whether you’re truly ready for retirement.

If you’re considering retiring at 55, a comprehensive financial plan can help you evaluate your options, identify potential risks, and determine whether early retirement aligns with your long-term goals.

The sooner you begin planning, the more flexibility you’ll have when deciding when, and how you retire.

FAQs

Possibly. Whether $1 million is enough depends on your spending needs, other income sources, healthcare costs, and retirement timeline. Someone spending $40,000 per year may have very different needs than someone spending $100,000 per year.

Not necessarily. Many individuals retire successfully at 55, but doing so requires careful planning because you’ll likely need to fund several years before Medicare and Social Security benefits become available.

For many early retirees, healthcare costs and generating income before Social Security begins are among the most significant challenges.