One of the most common questions we hear is, “Am I on track financially?”

Whether you’re just starting your career, raising a family, or approaching retirement, it’s natural to wonder how your savings compare to others. While there is no one-size-fits-all answer, having general savings benchmarks can help you evaluate your progress and identify areas for improvement.

The key thing to remember is that financial success isn’t determined by comparing yourself to your neighbors or coworkers. Your ideal savings goal depends on factors such as your income, lifestyle, retirement goals, and future expenses.

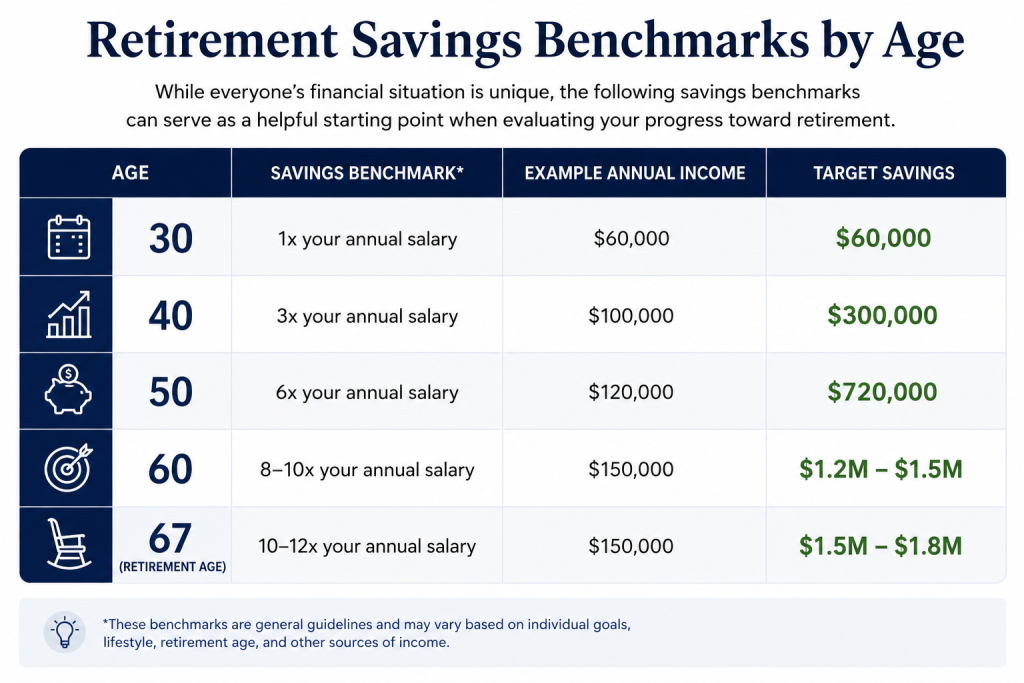

While everyone’s financial situation is unique, the following retirement savings benchmarks can serve as a helpful starting point when evaluating your progress toward retirement.

That said, let’s look at some commonly used savings milestones by age

Quick Note: These benchmarks are general guidelines based on annual income and may vary depending on retirement goals, lifestyle expectations, pension income, Social Security benefits, and other financial resources.

By Age 30: Build a Strong Foundation

Your 20s are often filled with major life events, starting a career, paying off student loans, buying a home, or starting a family. While it may be difficult to save aggressively during this stage, establishing good financial habits can have a significant impact over time.

A common guideline suggests having approximately one year’s salary saved by age 30.

For example:

- Annual income: $60,000

- Target savings by age 30: $60,000

If you’re not quite there, don’t panic. The most important factor at this stage is creating a consistent savings and investing strategy. Time is one of your greatest financial assets, and even small contributions can benefit from decades of compound growth.

By Age 40: Accelerate Wealth Building

By your 40s, your earning potential is often higher than it was earlier in your career. This can be an ideal time to increase retirement contributions and focus on long-term wealth accumulation.

Many financial planners recommend having approximately three times your annual salary saved by age 40.

For example:

- Annual income: $100,000

- Target savings by age 40: $300,000

At this stage, it’s also important to evaluate:

- Retirement account contributions

- Emergency savings

- Insurance coverage

- College funding goals

- Debt management strategies

Your 40s can be a critical decade for financial planning because the decisions you make now may significantly impact your retirement readiness later.-

By Age 50: Prepare for the Home Stretch

As retirement becomes more visible on the horizon, many individuals begin to take a closer look at whether they’re truly on track.

A common benchmark is to have approximately six times your annual salary saved by age 50.

For example:

- Annual income: $120,000

- Target savings by age 50: $720,000

This is also an excellent time to take advantage of catch-up contributions available through retirement accounts. These additional contribution opportunities can help accelerate savings during your highest earning years.

Beyond accumulation, investors should begin considering:

- Future retirement income needs

- Tax planning opportunities

- Social Security strategies

- Healthcare costs in retirement

By Age 60: Focus on Retirement Readiness

As retirement approaches, the conversation often shifts from saving money to creating a sustainable income strategy.

A general guideline suggests having approximately eight to ten times your annual salary saved by age 60.

For example:

- Annual income: $150,000

- Target savings by age 60: $1.2 million to $1.5 million

However, the amount you need depends on your desired retirement lifestyle. Someone planning extensive travel may require more savings than someone with a modest spending plan.

This is also the stage where many investors begin evaluating:

- Withdrawal strategies

- Required minimum distributions (RMDs)

- Tax-efficient income planning

- Medicare decisions

- Legacy and estate planning goals

Why Savings Benchmarks Don’t Tell the Whole Story

While age-based benchmarks can provide useful guidance, they don’t account for the complete picture.

For example:

- A person with a pension may need less saved than someone relying entirely on personal investments.

- A homeowner with no mortgage may have significantly lower retirement expenses.

- Someone planning to work longer may require less accumulated wealth than someone retiring early.

That’s why focusing solely on a savings number can be misleading.

Instead, it’s important to evaluate your overall financial plan, including your retirement goals, income sources, investment strategy, tax situation, and future expenses.

The Bottom Line

Savings milestones can serve as helpful checkpoints throughout your financial journey, but they should not be viewed as pass-or-fail benchmarks.

Whether you’re ahead of schedule, behind, or somewhere in between, the most important step is understanding where you stand today and developing a plan for where you want to go.

A well-designed financial plan can help turn uncertainty into confidence and provide a clearer path toward achieving your long-term goals.

If you’re wondering whether you’re on track for retirement, working with a financial professional can help you evaluate your current situation and build a strategy tailored to your unique goals and circumstances.

FAQs

The answer depends on your income, spending habits, and retirement goals. For someone earning $60,000 per year, $100,000 in retirement savings may represent strong progress. However, for someone earning $150,000 annually, additional savings may be needed to stay on track.

Rather than focusing on a specific dollar amount, it’s often more helpful to evaluate whether you’re saving consistently and making progress toward your long-term retirement objectives.

There is no universal target that applies to every couple. Factors such as retirement age, lifestyle expectations, healthcare expenses, pensions, Social Security benefits, and desired legacy goals can all impact the amount needed.

Many financial professionals recommend that couples aim to have between 10 and 12 times their combined annual income saved by retirement. However, the most accurate way to determine your target is through a personalized retirement income plan.

Retirement savings can vary significantly from one household to another. While averages can provide perspective, they don’t necessarily indicate whether someone is financially prepared for retirement.

What’s often more important is comparing your progress against your personal goals rather than national averages. A comprehensive financial plan can help determine whether your current savings strategy aligns with the retirement lifestyle you envision.