Retirement investing can feel intimidating when you first start hearing terms like 401(k), Roth IRA, stocks, ETFs, and compound interest. Many people assume investing is only for financial experts or wealthy individuals, but the reality is much simpler. Retirement investing is really just the process of consistently putting money away today so it can grow and support you later in life.

The earlier you understand the basics, the easier retirement planning becomes. You do not need complicated strategies or advanced financial knowledge to get started. In fact, many successful retirement plans are built on a few simple principles followed consistently over time.

This guide breaks down retirement investing in simple, beginner-friendly language so you can better understand how it works and why it matters.

Why Retirement Investing Matters

One of the biggest misconceptions people have is believing they can simply save money in a bank account for retirement. While saving is important, inflation slowly reduces the purchasing power of cash over time. That means the money sitting in a regular savings account today may not buy nearly as much in 20 or 30 years.

Investing helps your money grow over time in a way that has historically outpaced inflation. The goal is not to get rich overnight. The goal is to allow your money enough time to compound and grow steadily throughout your working years.

For example, someone who starts investing in their 20s often has a major advantage over someone who waits until their 40s, even if the younger investor contributes less money overall. Time is one of the most powerful tools in retirement planning.

What Does Investing Actually Mean?

Investing simply means purchasing assets that have the potential to increase in value over time.

Common investment types include:

- Stocks

- Bonds

- Mutual funds

- ETFs (Exchange-Traded Funds)

- Real estate investments

When you invest, your money is working for you instead of sitting idle. Some investments generate growth through increasing value, while others may provide income through dividends or interest payments.

Although investments can fluctuate in the short term, retirement investing is designed to focus on long-term growth over decades rather than daily market movements.

Understanding Retirement Accounts

One of the most important parts of retirement investing is understanding the accounts available to you.

401(k) Plans

A 401(k) is an employer-sponsored retirement account that allows employees to contribute money directly from their paycheck.

One major advantage of a 401(k) is that many employers offer matching contributions. For example, if your employer matches up to 5% of your salary, contributing enough to receive the full match is essentially free money toward your retirement.

401(k) accounts also provide tax advantages that can help your investments grow more efficiently over time.

Roth IRA

A Roth IRA is an individual retirement account funded with money that has already been taxed.

The major benefit is that qualified withdrawals during retirement are generally tax-free. This can be especially valuable for younger investors who expect their income and tax rates to increase over time.

Roth IRAs are popular because they combine long-term investment growth with potential tax-free retirement income.

Traditional IRA

A Traditional IRA works similarly to a Roth IRA, but the tax treatment is different.

Contributions may be tax-deductible today, but withdrawals in retirement are typically taxed as income.

Both Roth and Traditional IRAs can play important roles in a retirement strategy depending on your financial situation and long-term goals.

What Are Stocks?

Stocks represent ownership in a company.

When companies grow and become more profitable, their stock prices may rise over time. Investors can benefit from that growth through increased share values and, in some cases, dividend payments.

While stock prices naturally rise and fall, the overall stock market has historically grown significantly over long periods. That long-term growth is one reason stocks are commonly used in retirement portfolios.

However, stocks also come with risk, which is why diversification is important.

Understanding Diversification

Diversification means spreading your investments across different assets instead of relying on one single investment.

Rather than putting all your money into one company or industry, diversification helps reduce risk by distributing investments across many companies, sectors, and asset types.

Many retirement investors use mutual funds or ETFs because they provide built-in diversification by holding large groups of investments within a single fund.

This helps simplify investing while reducing exposure to the performance of any one company.

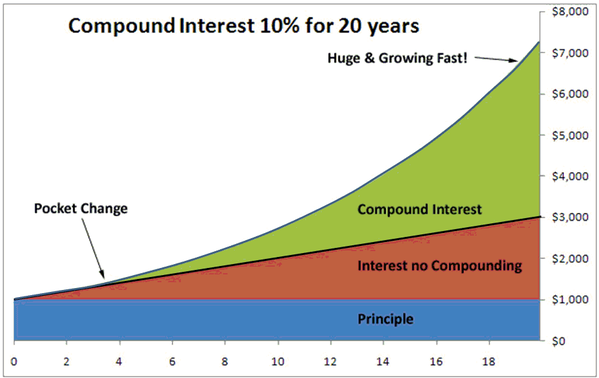

The Power of Compound Growth

One of the most important concepts in retirement investing is compound growth.

Compound growth occurs when your investment earnings begin generating earnings of their own over time.

This is why starting early matters so much. Even small contributions made consistently over long periods can potentially grow into substantial retirement savings.

Many investors are surprised to learn that consistency and time are often more important than trying to find the “perfect” investment.

Understanding Risk and Market Volatility

All investments involve some level of risk. Markets naturally experience periods of growth and decline.

One of the biggest mistakes beginner investors make is reacting emotionally during market downturns. Short-term volatility is normal, but retirement investing focuses on long-term trends rather than temporary fluctuations.

Historically, markets have recovered from downturns over time. Investors who remain disciplined and continue contributing consistently are often better positioned for long-term success than those who constantly move money in and out of investments.

How Much Should You Invest?

A common guideline is to contribute around 10–15% of your income toward retirement if possible. However, the most important step is simply getting started.

Even small monthly contributions can make a meaningful difference over time. Waiting for the “perfect time” to invest often results in lost years of potential growth.

Retirement investing works best when contributions become a consistent habit rather than an occasional decision.

Common Retirement Investing Mistakes

Even simple retirement plans can run into problems if investors are not careful.

Some common mistakes include:

- Waiting too long to start investing

- Ignoring employer 401(k) matching contributions

- Trying to get rich quickly

- Taking excessive risk

- Panicking during market downturns

- Keeping all retirement savings in cash

Successful retirement investing is usually built through consistency, patience, and long-term discipline rather than short-term speculation.

Bringing It All Together

Retirement investing does not need to be overly complicated. At its core, it comes down to consistently saving money, investing for long-term growth, and allowing time and compound growth to work in your favor.

Your retirement accounts provide tax advantages.

Your investments provide long-term growth potential.

And your consistency provides the foundation for long-term financial security.

The most important step is simply starting. You do not need to know everything before beginning, and you do not need a perfect strategy right away. Building retirement wealth is a long-term process that improves over time as your knowledge and experience grow.

With the right habits and a basic understanding of investing principles, retirement planning can become far less intimidating and much more achievable.

FAQs

Retirement investing is the process of putting money into investments like stocks, mutual funds, ETFs, and retirement accounts to help grow your wealth over time and provide income during retirement.

Investing is important because inflation can reduce the value of cash over time. Investments have the potential to grow faster than traditional savings accounts and help build long-term financial security.

Many beginners start with a 401(k) through their employer or a Roth IRA. Both offer tax advantages and can help grow retirement savings over time.